Two weeks ago, diesel was trending down. The EIA's national average sat at $3.71 a gallon in mid-February, and forecasters, the EIA included, were calling for sub-$3.50 averages through most of 2026. Carriers were cautiously optimistic. After three brutal years of margin pressure, cheaper fuel looked like it might finally give them some breathing room.

Then the bombs fell.

On Feb. 28, joint U.S.-Israeli strikes hit Iran, killing Supreme Leader Ali Khamenei. Iran retaliated with missiles and drones aimed at Israeli territory and U.S. bases in the Gulf. The Islamic Revolutionary Guard Corps declared Hormuz closed to vessel traffic. Within days, tanker movements through the strait dropped roughly 70%, with more than 150 ships anchoring outside the chokepoint. Tehran has since walked back the language, saying it hasn't formally closed the strait but will block U.S.- and Israeli-linked ships from transiting. The distinction is largely semantic. Commercial traffic has fallen to near zero.

The Strait of Hormuz handles about 20% of the world's daily oil supply. That's a bottleneck the global market can't route around quickly.

What happened to diesel

Diesel futures jumped 12% in the first trading sessions after the strikes. The EIA's weekly average climbed from $3.71 to $3.90 a gallon by March 3, a 19-cent jump in roughly two weeks and the highest national average since April 2024. Brent crude, which had been hanging around the mid-$60s, blew past $80 and kept climbing. By March 6 it was trading near $90, a 24% surge since the war began. Morgan Stanley raised its oil price forecasts this week, citing a Hormuz risk premium that shows no sign of fading. Barclays told clients $100 a barrel is plausible if the security situation keeps spiraling.

Before the conflict, the outlook was soft. Global crude inventories were healthy. OPEC+ was gradually unwinding production cuts. The EIA's February outlook projected diesel averaging $3.50 a gallon for 2026. That forecast assumed no major supply disruptions.

It assumed wrong.

How bad could this get?

Six weeks ago, the analysts covering diesel markets were bored if anything. Inventories were stable, demand was predictable, and the biggest variable on anyone's model was whether OPEC+ would add another 100,000 barrels a day. Now those same analysts are running war scenarios, and their models are spitting out numbers that don't agree with each other.

If the strait reopens within weeks — Trump has offered insurance and escorts for tankers transiting the Gulf — prices probably settle back toward the mid-$3 range for diesel. The market was soft enough heading in that a short disruption gets absorbed. (On Rig Load, the binary market Will diesel fall below $3.25 in Q2 2026 is testing whether anyone still believes in the pre-war trajectory. It's now effectively a freebie)

Sustained closure is a different animal. Some commodity analysts have modeled scenarios where months of Hormuz shutdown pushes Brent $40 to $80 above baseline. With crude already at $90, that arithmetic starts getting alarming: $130 a barrel is no longer a fringe scenario. Run that through the refining margin and you're looking at diesel north of $4.50 a gallon. Maybe above $5 in California and the Northeast, which always get hit hardest.

The most probable outcome, at least from where things stand this weekend, is messier than either extreme: sporadic disruption, tanker insurance premiums in the stratosphere, and a slow grind higher in crude as the market tries to price in a war with no clear end date. On trading desks, as NPR reported this week, prices are surging, but the market hasn't panicked yet. Diesel in the $4 to $4.50 range by early summer feels like a reasonable middle case, and that's a much darker picture than it was even two days ago, before Brent crossed $90.

What this means for trucking

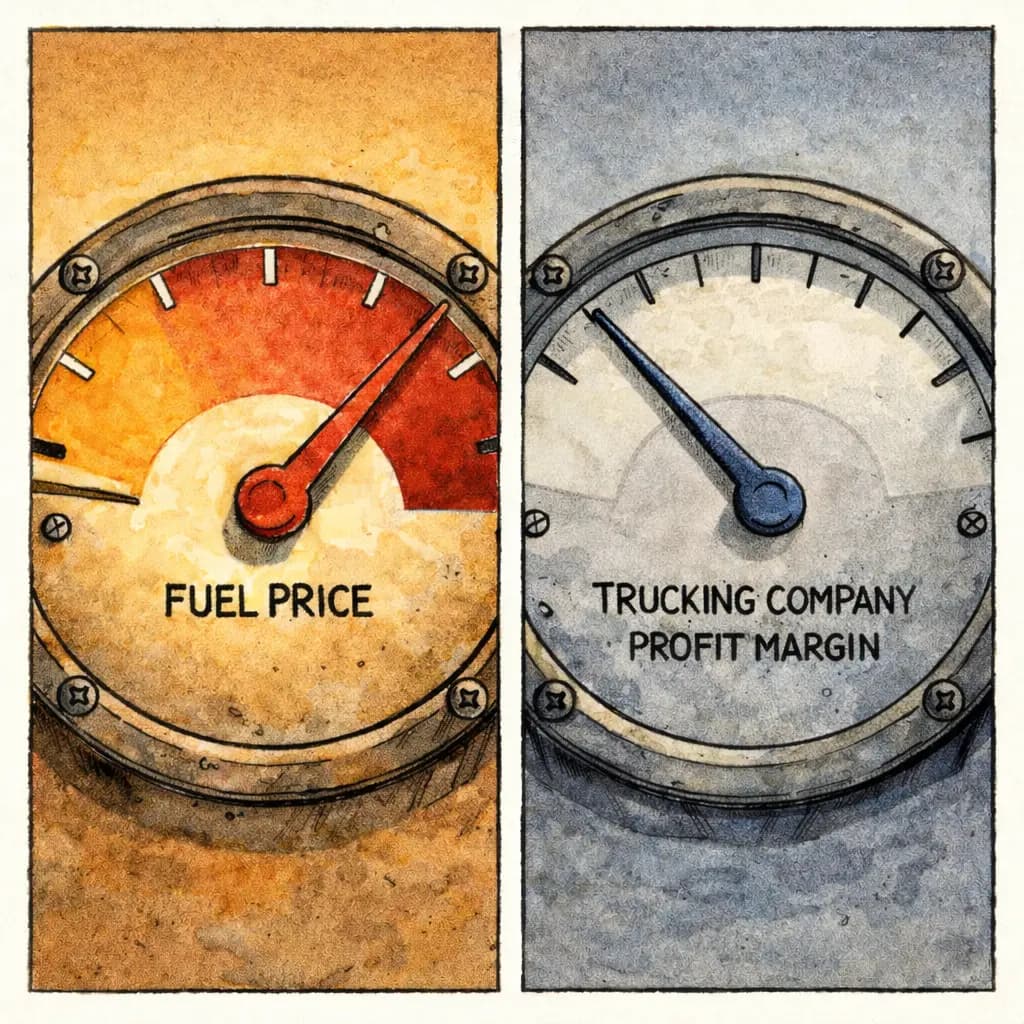

Fuel is roughly a quarter of a motor carrier's total operating costs. When diesel moves 20 cents in two weeks, carriers don't need an analyst to tell them.

The timing could hardly be worse. Spot truckload rates have been climbing. According to DAT Trendlines, national van rates hit $2.41 a mile in February. Reefer freight averaged $2.88. Year over year, spot rates were running a few percentage points higher in early February. For a carrier glancing at the spot board, that was starting to look like a recovery. Now it's more complicated.

Contract rates, where most carriers make their real money, have barely budged. Shippers are holding firm in bid season, offering low-single-digit increases at best. Meanwhile, operating costs keep climbing: insurance, maintenance, driver pay and now fuel. The revenue-to-cost gap on contract freight is getting tighter by the week. A lot of carriers are hauling more loads and making less money on each one.

Fuel surcharges exist to protect carriers from exactly this kind of volatility, but surcharges are a lagging mechanism by design. Most are pegged to the weekly EIA diesel average and reset on a delay. When prices spike quickly, carriers eat the difference for days or weeks before the surcharge catches up. And surcharges never cover 100% of the actual cost increase. They're calculated on loaded miles, but trucks burn fuel deadheading, idling, running the APU and sitting in detention. The margin disappears in that gap between what the surcharge reimburses and what the truck actually burns.

Small carriers and owner-operators feel this the most. They have less cash to absorb a sudden $200-a-week increase in fuel spend and less leverage to negotiate terms. A sustained diesel price above $4 would push some marginal operators out of the market. Industry projections suggest capacity could shrink another 3% to 5% by mid-year even without a fuel shock; layer one on top and the exits accelerate. That would eventually tighten capacity and push rates higher, but not before some damage gets done. How much damage, and how wild the price swings get in the meantime, is exactly what another Rig Load market on diesel volatility in 2026 is trying to answer.

(This is another freebie, as the percentage change is likely to move above 15% with the next EIA reading.)

Where things were headed before Iran

It helps to remember what the freight market looked like a month ago.

The freight recession that started in late 2022, the longest in modern memory, had finally started to ease. Spot rates were recovering. Tender rejections were ticking up, a sign that carriers had clawed back some pricing power. Diesel had been drifting lower for months. The EIA was projecting a 7% decline in diesel prices for 2026 compared to 2025.

The industry was in the early innings of a cyclical recovery. Not a boom. Almost nobody was calling it a boom. But a slow, grinding crawl back toward equilibrium after years of excess capacity and depressed rates. Carriers that white-knuckled their way through the downturn were supposed to be rewarded with a tighter market and lower input costs.

The Iran conflict doesn't kill that recovery. Freight demand is still holding up. But it rewrites the terms. Instead of margin improvement from falling fuel costs, carriers are staring at margin compression from rising fuel costs at the exact moment when contract rates haven't caught up. As FreightWaves noted this week, the war is layering a fuel crisis on top of an industry that was already stretched thin. The recovery still happens, probably, but it'll be harder and slower than anyone expected a month ago.

The EIA's pre-war projection had Q2 diesel averaging $3.41. That number is already stale. The question is how stale. A quick resolution at Hormuz and you're probably in the $3.50 to $3.70 range. Persistent disruption or escalation puts you north of $4. The real bears are looking at $4.50 or higher, and with Brent already at $90 and climbing, they're not crazy.

Three months out, with an active military conflict in a region that controls a fifth of global oil flow, the range of plausible outcomes is enormous. Anybody can predict diesel when the trend line is smooth. Predicting it through a war is where you find out who actually reads the market and who was just riding the curve.

What to watch

Any credible sign that the strait is reopening, even partially, even under military escort, will take $5 to $10 off Brent almost immediately. The oil market is pricing in maximum fear right now, which means the downside on any de-escalation headline is just as dramatic as the upside was on the first strike.

The SPR is the other lever, but it's looking unlikely. The president ruled out a release as of March 4, and energy advisers have warned that a failed or insufficient intervention could rattle markets. The reserve holds about 415 million barrels, a little more than half its capacity. If the administration reverses course and starts selling, that takes the sharpest edge off the spike. But it doesn't fix the underlying supply problem, and the political appetite for it appears thin.

Meanwhile, Maersk rerouted its Middle East services around the Cape of Good Hope, adding 10 to 14 days and roughly 40% more fuel per voyage. Oil keeps flowing, but at a serious premium. The longer the strait stays closed, the more the market adjusts to these longer routes, and the less dramatic each subsequent week of closure becomes.

U.S. diesel inventories were in decent shape coming into this. If they hold, retail prices have a ceiling. If draws accelerate because refiners can't source enough feedstock, the ceiling comes off.

For trucking specifically, the EIA's weekly report is your leading indicator for fuel surcharge resets. Keep an eye on tender rejections on DAT and SONAR too. If small carriers start exiting and capacity tightens, the rate picture changes fast.

Make your call

The old diesel forecast is broken. The new one depends on variables that are as much political as economic, and the situation could shift in either direction any given week.

If you've got a read on where this lands, put it on the board. The diesel forecast on Rig Load is open. Your prediction, your reputation.