Much of freight has been mired in a downcycle for three years. Carriers have struggled with compressed margins. Brokers have watched volumes thin out. Shippers have held the upper hand on pricing for the better part of a cycle that, by most historical measures, already should have turned.

But heading into spring 2026, a handful of indicators suggest something is shifting. It looks less like the sharp correction many expected and more like a slow grind, compounding quietly enough that it's easy to miss entirely.

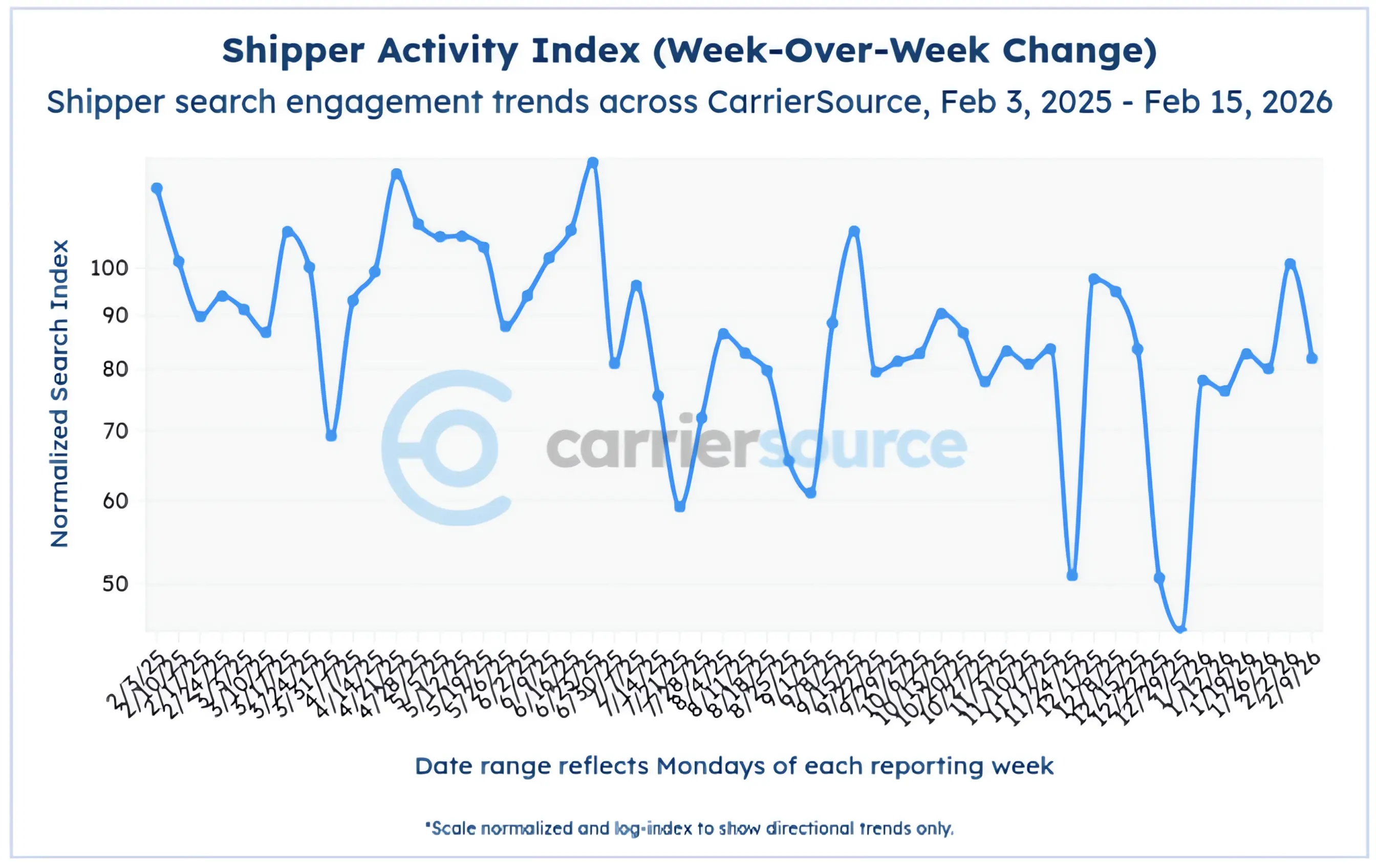

One telling measure is the CarrierSource Shipper Activity Index, which tracks how aggressively shippers are sourcing carriers on the platform. The index functions as a proxy for the tension between freight demand and available capacity: when shippers have to work harder to find coverage, the reading climbs.

Because the index moves in sharp weekly swings, the more useful analytical lens is the four-week rolling average, which smooths out the noise and surfaces the underlying trend. On that basis, the index peaked at 108.39 in the rolling period ending Feb. 24-March 2 of 2025, inflated in part by front-loading as shippers rushed to move freight ahead of expected tariff action. That was pulled-forward demand, not purely organic growth. By the week of March 17-23, the four-week rolling average had settled to 89.66. Days later, the reciprocal tariff announcements sent the market into a tailspin and the index collapsed to the low 70s.

A year later, the four-week rolling average ending Feb. 9-15, 2026 stands at 89.81. The smoothed trend is running almost exactly even with where it stood at this same point in 2025. Spring shipping season is approaching. The central question is whether the rolling average will hold or build through March, and what the answer means for the balance of the year.

The Question

Will the four-week rolling average of the CarrierSource Shipper Activity Index for the period ending March 22, 2026 exceed 89.66?

During the same four-week window in 2025, the rolling average stood at 89.66. The current four-week rolling average, as of Feb. 9-15, 2026, is 89.81 — essentially flat with last year's benchmark. A reading above 89.66 would indicate that the smoothed demand and capacity trend is running at or above last year's pre-tariff pace. A reading at or below it would suggest the market has softened from where it stood heading into last spring.

Resolves YES if the four-week rolling average exceeds 89.66. Resolves NO if the rolling average reads at or below 89.66. Source: CarrierSource.

Kevin Hill has spent years in freight brokerage and market data. He currently serves as head of sales at CarrierSource, where he works directly with the shipper activity data behind this question. He also runs Brush Pass Research, a freight market intelligence firm. We talked with Hill to get his read on what the index is telling us heading into spring.

Index values referenced in the Q&A below reflect weekly readings at the time of the interview in early February 2026. The market question and surrounding analysis use four-week rolling averages for a smoothed view of the underlying trend.

Q: The Shipper Activity Index sits at 82 right now. Last year at this time it was considerably higher. What does that tell you about where we are?

Last year, that second week of February was the high mark. The index was at 136. By mid-March it was 108, and that was right before the reciprocal tariffs were announced and put in place. That week it dipped from 108 to the low 70s. So last year's March reading accounted for some front-loading. It was a more dramatic shift. We're approaching that same window now, and the question is: is it going to be stronger, muted, or about the same compared to last year?

Q: What are the strongest signals you're watching that suggest a tighter market is coming?

On the capacity side, the non-domiciled CDL announcements and enforcement, that's been compounding. The closure of driving schools feeds into it. On the equipment side, four years ago, a five-year-old semi was $150,000 on the used market. Now that's way down, and people who bought in have struggled through this downcycle. No one's adding capacity. From new truck sales, you can see that fleets have been delaying purchases. There's not a lot of new equipment coming onto the scene.

And then on the demand side, the ISM was up big last month. You've got energy companies with stock rising, data center construction from the tech companies. Those are projects in process and new ones coming online. There's supposed to be larger tax refunds coming in. Any of those things that spur demand could make it a very hot market.

Q: What would have to happen for a bull case to play out this spring?

The non-domiciled CDL stuff has to be sticky, and it has to remove a good chunk of capacity. Same with English language proficiency enforcement. All of this feeds into it. And then on the demand side, it's the things we've been talking about. You've got AI-driven CapEx building from the tech companies, great commercial and industrial construction, which is great for trucking. If capacity is tight and any of those demand catalysts kick in, it could be a very different year than what we've seen over the last three.

Q: What are the bears getting wrong?

They're missing the slow buildup that's happening right now. They're discounting it and thinking that since it didn't happen quickly, it's not going to happen, that it's going to be another false run. There's a lot of people in freight who aren't bought into market swings until the very end.

The non-domiciled and ESL enforcement, they came out with those announcements months ago and nothing really changed in the market right away. But it's taking time for it to compound. If you're bearish, you don't think it's going to have that much of an effect. On the demand side, you're much more bearish about the economy. A recession kicking in, slower growth. You're looking at things like January being the slowest new home sales in four or five years, debt levels out of control. There are ways you can paint the economy as bearish. But I think the slow buildup is something we haven't seen in a while.

Q: How would you describe your own outlook?

I'm an optimistic realist. I won't make a bold call or anything, but I can see the puzzle pieces coming online to where it is going to be a much different year than what we've seen over the last three years. Throw in tax refunds, anything that spurs demand, it could make it a very hot market. What that will be down the road, I have not a clue, but oftentimes it comes out of the blue, out of left field. I'd say I'm a little bit more bullish.

The Forecast

Hill's call:

Yes. The capacity-side pressures are compounding and the demand signals, from ISM to construction CapEx, suggest this spring will be meaningfully stronger than last year's pre-tariff baseline.

Rig Load tracks forecasting accuracy over time. Build your reputation by going on the record.

About Kevin Hill

Kevin Hill is a freight-tech entrepreneur and market analyst, founder of Brush Pass Research, and a longtime operator in the freight brokerage ecosystem. He currently serves as head of sales at CarrierSource, where he leads growth initiatives focused on real-time shipper intent data and AI-driven prospecting solutions.